1. Customs duties

Customs duties or customs are duties that are paid on customs goods upon import into the EU.

Customs duties are the most widespread instrument for protecting the domestic economy. As goods become more expensive and thus indirectly reduce imports from abroad, domestic products are more attractive to buy. Customs duties are also a source of funds for filling the state budget.

Definition of customs terms:

All goods carried or transported through the customs territory. A distinction is made between Community goods (within the EU) and non-Community goods (goods from third countries coming into the EU under customs control).

Territory where the same customs duties and the same customs regulations apply. The customs territory of the Community (EU) is the territory of the Member States with the exception of third territories (Faroe Islands, Ceuta and Melilla) and including countries outside the EU (Monaco and San Marino).

An enclosed space for which the warehouse-keeper holds a permit for the storage of customs goods.

All customs regulations, which determine customs control, the customs procedure, customs clearance of goods and regulate the rights and obligations of persons in the customs procedure.

- Single Administrative Document - SAD:

A document with which the declarant declares the goods for customs clearance in the prescribed form and in the prescribed manner with import or export transactions.

- Export Accompanying Document - EAD:

A document marked MRN, which is printed from the computer system by the customs office of export after acceptance of the electronic export declaration and release of the goods for export.

- Movement Reference Number - MRN:

The number under which the SAD is entered in the SIAIS Customs System. Based on this number, the shipment can be identified in the Customs System. It comprises of a unique sequence of 18 characters, which are automatically determined by the Customs Information System upon receipt of the SAD

The person who draws up the customs declaration and lodges it with the customs authority on their own behalf or on behalf of the contracting authority (the person importing or exporting the goods).

The EORI number is the identification number of the economic operator used for customs purposes. It is valid throughout the EU and is a condition for customs operations. Economic entities obtain an EORI number in their respective country, in Slovenia it is assigned based on the VAT number. Customs Administration of the Republic of Slovenia - Jesenice Customs Office is in charge of registration.

A customs tariff is a system of numerical codes used to identify each item under a customs procedure. On the basis of this system, the rates at which customs duties are calculated and paid are determined. In the EU, this task is performed by TARIC.

Percentage of ad valorem duties or nominal value of specific duties, expressed as the amount of duty payable on a good.

The value of goods used as a basis for calculating customs duties on the basis of rates from the customs tariff or for the calculation of VAT. The customs value includes all costs until the goods enter the EU (transport costs, costs of intermediaries, commissions, royalties…)

Import customs procedure for the presentation of goods, lodging of a customs declaration, settlement of a customs debt and release of goods for free circulation.

- Release of goods for free circulation:

The action of the customs authorities by which they release the goods during the import procedure when the duties have been paid or secured.

It arises from the release to free circulation of imported goods subject to import duties or from the entry of such goods for the temporary admission of goods. It arises at the time of the release of the SAD.

2. The EU customs system

The EU has unified the foreign trade policy of the Member States, which is implemented throughout the EU.

This means that the EU acts externally as one country, which makes it easier to do business with third countries in import and export transactions. The movement of goods between Member States within the EU itself is a duty-free movement,

Legal references and legislation governing customs:

- Union Customs Code,

- Act Implementing the Customs Regulations of the European Community (ZICPES),

- Customs Service Act (ZCS),

- Tax Procedure Act (ZDavP),

- Value Added Tax Act (ZDDV).

Origin of goods

The Generalized System of Preferences or GSP is an EU foreign trade policy instrument designed to encourage imports from developing countries. The GSP establishes a total or partial exemption from customs duties on imports into the European Community of goods originating in developing countries. Preferential means priority, favorable. Companies have savings in the amount of customs duties and lower tax.

Difference between preferential and non-preferential origin of goods:

Preferential origin of goods allows customs benefits (lower customs rates) for imported goods, while non-preferential origin only tells which country the goods come from, but customs benefits do not apply to them.

Rules on the preferential origin of goods can be found in the Union Customs Code, in trade agreements between the EU and certain countries, and in autonomous preferential arrangements.

When exporting or importing goods, companies must provide the customs offices with proof of the preferential origin of the goods on prescribed official forms.

Proof of origin forms:

Proof of the origin of goods in trade with countries with which the EU has concluded trade agreements or autonomous preferential arrangements.

Proof of origin in trade with Syria for shipments worth EUR 850.The certificate is issued by the exporter and is not validated by the customs authorities.

Proof of origin in trade with countries involved in the pan-Euro-Mediterranean cumulation of origin of goods.

It applies to imports from developing countries under the EU's Generalized System of Preferences.

- Simplified certificates of origin:

Declaration of the exporter on an invoice in the value of up to EUR 6,000, statement of the authorized exporter on an invoice over EUR 6,000, statement of the authorized exporter on the EUR-MED invoice declaration. The text is defined in detail.

Intrastat - Extrastat

Companies are required to report on the dispatches and arrivals of goods within the EU on a monthly basis:

- Intrastat is statistics on trade in goods between EU Member States. All companies whose total trade in goods in the EU has exceeded the so-called assimilation threshold (EUR 200,000 for the dispatch of goods and EUR 140,000 for the arrival of goods) are obliged to report. Taxable persons must send the report by every 15th of the month for the previous month. The authorized customs office for Intrastat is the Nova Gorica Customs Office, which is obliged to report to Eurostat Brussels by every 30th of the month for the previous month.

- Extrastat is statistics on the trade of EU Member States with non-EU third countries. The source of data is the Single Administrative Document (SAD).The extract does not have an assimilation threshold and all data must be captured.

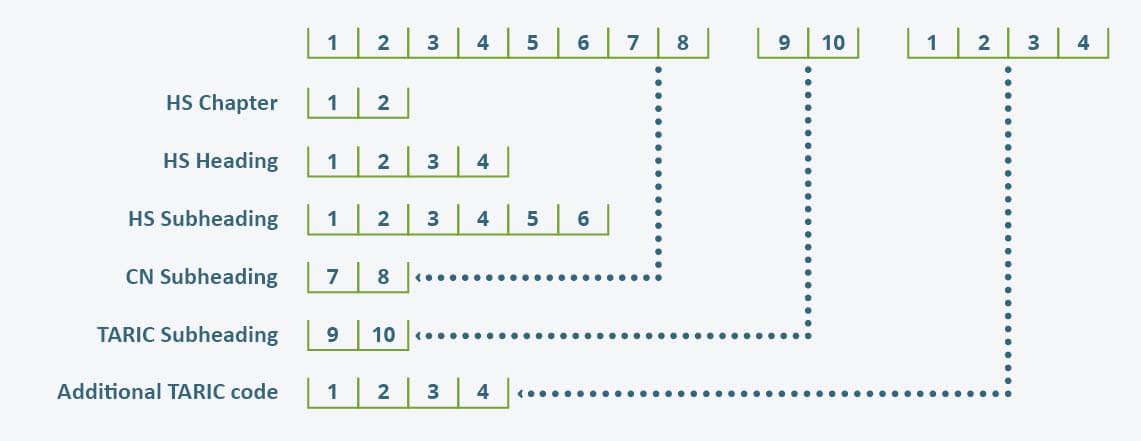

TARIC

The condition for the functioning of the customs union and the EU common market is the uniform application of foreign trade rules in all Member States. This unity is provided by TARIC − the integrated tariff of the European Community. The TARIC is a systematically arranged list of goods containing tariff codes, tariff names and customs rates.

Code structure:

The Common Customs Tariff TARIC is used for trade with third countries and is uniform throughout the EU. The level of import duties varies according to the type of goods and the country from which they are imported.

VAT

In the EU, value added tax (VAT) is considered a form of taxation, goods are taxed on imports and goods are exempt from VAT on exports.VAT is calculated and paid on the turnover of goods and services on the territory of Slovenia and on the import of goods into the EU.

The method of payment of VAT is governed by national law.

The supply of goods to another EU Member State is exempt from VAT in Slovenia if the following conditions are met:

- the seller is an identified taxable person in a Member State,

- the movement of goods is carried out for remuneration,

- the goods are produced in the territory of Slovenia,

- the consignee of the goods is an identified taxable person (valid VAT ID number of the buyer),

- it issues an invoice to its customer stating that VAT has not been charged,

- the buyer of goods in another Member State charges VAT in their own country at the applicable tax rate in that country.

In the case of purchases of goods from another Member State, VAT is charged and paid (with certain exceptions) under the following conditions:

- the supplier of goods in another Member State identified for VAT issues an invoice to the buyer in Slovenia stating that VAT has not been charged under a certain article of the law in force there,

- the movement of goods is carried out for remuneration,

- The Slovenian buyer - taxable person has to charge VAT on the 15th day after the month of delivery in Slovenia.

VIES

Every taxable person must check that its customers from an EU Member State are identified as taxable persons and that they have a valid VAT number. For this purpose, the VIES (VAT Information Exchange System) database has been set up, which contains all data on taxable persons, as well as information on the expiry of the VAT number.

For more information, contact [email protected] or read http://www.rcm.si/en/Customs-procedures/Transit-procedure